I have been asked many questions since we have openly shared about our journey to get out of debt and our goal to be self-reliant. We are middle-aged parents to a large family with four kids, and we had to learn a few tricks along the way to figure this whole “budgeting“ and “getting rid of our student loans for good“ thing out.

A frequently asked question James & I get is, “Where do I even start? How do I start a debt-free journey?!?!!”

There are many ways to start a debt-free journey.

Seriously, so so many ways to start.

If anyone ever tells you otherwise, know that that person is full of bologna.

What works for one person may not work for you. And that is 100% the way life was intended to be. How boring would it be if we ALL lived the same exact story?

I digress. Let me step off my soapbox and finish what I started to say.

There are many ways to start a debt-free journey. If you are looking for answers and general direction, here are 5 amazing things that helped us BEFORE we started working on our debt-free journey.

1.) Call A Household Meeting

If you are single, this obviously doesn’t apply to you. But if you are sharing finances with a partner (or even if your finances aren’t combined, but you split the bills), you need to call a household meeting. You both need to be on the same page regarding responsibilities.

Or to re-phrase:

You shouldn’t have to bear the burden of all the stress that finances can cause alone when you are part of a partnership.

Again, if you are similar to us, this can be a super-charged-easily-upset-and-uncomfortable meeting. Especially when facing hard truths like you have spending problems, aren’t saving enough, haven’t been smart with your investment choices, or have a mountain of debt to pay off.

This is especially true for people who feel budgets “tie them down” and feel restricting.

Try to meet together when you are feeling your best. Make sure you both are rested, well-fed, and postpone the meeting if you’ve had an incredibly stressful day with the kids or at work. I promise the subject of budgets and debt will still be there when you feel less overwhelmed.

Our budget meetings and discussions of “We need to spend less” could only go so far.

This leads me to step 2: What you should discuss at your household meetings.

(Hint: It will probably take several meetings to get real headway with your finances. Have the expectation that you won’t get all of this done at the first meeting. Give yourself time to perform them in steps and process changes that need to be made.)

2. Find Your Motivation

Why are you invested in paying off your debt? How would paying off your debt and being free of those minimum payments mean for your life? What would it mean for your family? Why do you care about budgeting and getting a handle on your finances?

Take time to brainstorm about what personally motivates you, and then talk together about it.

And realize before you even start that what motivates YOU might not motivate your PARTNER… and that is also 100% the way life is intended.

Again, how boring would life be if our partner wanted the same exact things as we did? I’ll answer for you – SUPER BORING! We’d never grow or stretch or learn. We’d never be exposed to new paradigms and options outside of our own blindspots and views without giving and taking.

When working with a partner, listen to what motivates them. Find out what their dreams are. Talk about the type of future you hope to have or the kind of future you’d love your family to have.

I’ll give you a little insight into how our pivotal “household meeting dream chat” went.

When James and I got married, I immediately had a goal to pay off the debt I had just inherited. He had car loans, credit card bills, and maybe $15,000 worth of student loans. Easy peasy, I thought. In a few years, we could have that gone.

Fast forward a decade, and I was STILL working to pay off our debt and dig ourselves out of the financial pit-of-despair that we lovingly call our “burning fire of crap” years.

It was frustrating to still be working on the same goal for a decade-plus. It was exhausting, and I was feeling defeated doing it on my own.

James will be the first to admit that in a decade of marriage, he never really followed a budget and didn’t like the idea of it. He likes spontaneity, fun, and freedom and felt a budget was the opposite of those things.

So James usually spent a lot of our budget meetings with glossy eyes, head nods, and unintentionally misleading promises to not overspend, but with no real conscious intention to change.

However, I am lucky to be married to a big dreamer who shoots for the stars, the solar system… and then the galaxy itself. (And the poor guy married me: a girl who can’t help but think worse-case-scenario for everything.)

We spent an entire week DREAMING.

Yep, an entire week.

He thought of every possible cool thing he wanted to experience. He thought of the expensive jeep he’s dreamed of since college and the camera equipment he wanted to own. He thought of adventurous retreats and once-in-a-lifetime foreign travels he could take. He thought of his kids and the fun experiences he’d love to have with them. Many of them were things I’d never even heard of. (In comparison, mine were things like visiting art museums and paying for our kids’ weddings & honeymoons. Like I said, to each their own.)

When I showed James how much money we had to pay towards debt every month and how much money would free up once we became debt-free, it was like a light switch went off in his head. He was able to see what a difference budgeting could make for our life, where we could stop wishing and start living our dreams.

What motivates YOU will be deeply personal and different. You have your own money blueprint with your own motivations. Take time to ponder and figure out WHY you want financial self-reliance and independence. And write “your why’ down where you can see it every day to remind you WHY you will work so hard on this goal.

I made a collage vision board with “my why” and use it as the background on my phone so I can see it everyday. (You can make your own in Photoshop or I bet Canva!)

Paying off debt is no walk-in-the-park. It takes a lot of discipline and sacrifice, so honing in on what is motivating you and WHY you are doing it will help keep you going through the thick of it.

3.) Calculate How Much Debt You Actually Owe PLUS How Much You Have in Savings

For some people, this may be easy. (Yay! That’s amazing!) But if you’re anything like us – finding out how much total debt you have will take some digging.

We had to sign in to four different banks to find all our loan and credit card amounts. Then we had to total up personal loans a parent gave us and our student loans – of which there were 10 different loans.

Talk about a cringe-worthy-wanna-throw-up-and-just-die moment.

You won’t want to do it.

You’ll want to avoid this at all costs.

But trust us. It’s a necessary step.

Before you come up with a plan or start, you have to know WHERE you currently are. Tally up how much debt you actually have. Write down a list of all the current debts you have. Sign in to those accounts and write down the total amount you owe on that debt. This would be a great time to write down important info such as minimum payments you have to make each month, the apr (interest) rate, and when those minimum payments are due.

Going hand-in-hand with knowing how much debt you have, you need to figure out how much savings you currently have available as well. This was much easier for us since we only had one saving account at the time. But if you have multiple investment and savings accounts, tally that total up, so you know your current savings amount.

4.) Dive Into Your Spending Habits

We highly suggest tracking your spending habits over the current month + the 2-6 months before. This will indicate how you handle your finances and be a big eye-opener into your spending habits.

(Note: If you have a lot of variable expenses that change month-to-month, you may want to review your spending habits over the year too. This is helpful if your paychecks differ month to month as well.)

Just like we mentioned before, there isn’t only one way to track your spending habits. There are many ways to do it.

You could review your bank and credit card statements if you rely primarily on debit and credit cards. You could check your bills and hold on to all your receipts and track them that way. If you take cash out for things, you could place a notepad in your car or open up a note in your phone to quickly jot down what that money was spent on.

The goal here is to be specific and not just “guess” how much things are costing you, but review the facts of your actual expenses.

Keep an ongoing list of the category items you are spending money on and include how much each expense costs. Some of those items will come sporadically and others frequently. Make a note of when those charges were made and when all your recurring bills are due. (It will come in handy when reviewing or setting up your budget.) I write the due date next to my listed expense if it has one, but I know many people like to print out a generic calendar to keep track of their bills. Either one would work great for keeping track of when you need to pay your bills (& be prepared for it).

Make a note of any red flag spending habits that you might notice. These are purchases you don’t remember making, memberships you forgot you still had or being double charged for something. This could also be a great opportunity to flag items you don’t care about or use and don’t necessarily want to spend money on.

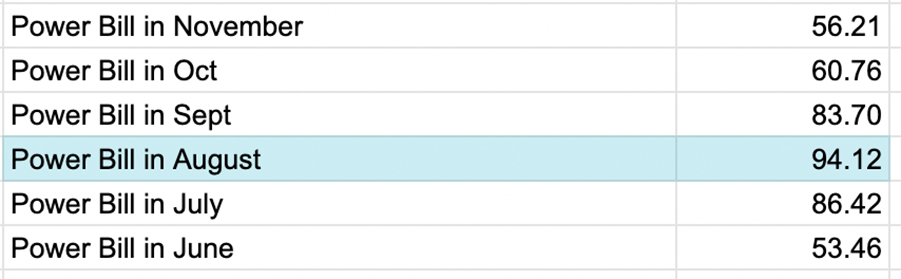

When tracking and factoring in irregular bills and expenses that you have every month, I generally look at how much we spent over the previous months and budget based on the highest month. This way, I should have enough to cover the bill and hopefully not take any money from savings.

Here’s an example of tracking our power bill, which is an irregular expense for us:

I know other people suggest finding the average amount you spend with variable spending, and on months you pay less than the average amount, save that money to be used for a higher-than-average month. (I find that a step too complicated for me, but it generally works if you have a small sinking fund you can throw your savings into to help pay for the higher-spending months.)

Here’s an example of how to factor the average number with your budget. I add the sum of the amount and divide it by the total number of months you tracked (values in the set).

I also suggest keeping track of other irregular expenses (such as membership fees, HOA fees, taxes, subscriptions, Christmas, Birthdays, Holidays, vet visits, etc.) so you know how much to expect those items to cost you and you can make a plan with your budget on how to cover those expenses without having to stress out or go into debt over them.

5.) Get Organized

Before you dive into creating or fine-tuning your budget and coming up with a plan to pay off debt, take time to get organized.

Please make a list of all your monthly expenses and separate them into budget categories. Calculate how much you have spent in each category and put that amount next to your listed costs. I like to clump fixed expenses (mortgage, subscriptions, insurance, fees, etc.) with variable, irregular expenditures (minimum payments, groceries, gasoline, etc.).

Next, organize the list you have of expenses that don’t happen every month. These could be expenses related to birthdays, holidays, insurance, taxes, vacations and traveling, vet visits, etc.

And lastly, before you start tinkering with your budget, I want you to make a third list – this time prioritizing all the above. Split the categories into Needs and Wants. When you were tracking your spending habits, you may have already flagged some items that aren’t important to you. Make sure that those flagged expenses are added to the lowest priority section of your needs and wants lists. And if you are really motivated to start a debt-free journey, make sure paying extra towards debt is at the tops of your needs list.

I suggest taking time and talking through with your partner together because what you consider a want might be a high-value expense for them that feels more like a need, and vice-versa. It would help if you worked together as a team. Take time to discuss this again when you are both in a good head-space. (For us, this usually means we are well-rested, well-fed, and well-loved).

I know it can be a lot of work to figure out personal finances and find a system that works for you. I hope this can get the ball rolling to give you some ideas of starting on a debt-free journey or getting a better handle on your budget.

I can’t promise it will be easy, but I can promise it will be worth it. Keep trying. Keep showing up. And keep tweaking and trying new ways to do things if what you are trying isn’t working for you.

Do you have any tips to getting started with a budget or debt-free journey that I missed? Please share in a comment below. I’d love to hear from you.

Looking for even more budgeting and debt-free tips?

We’re Debt Free! How We Celebrated & Surprised The Kids!

5 Changes We’ve Made Since Becoming Debt-Free

Our Debt-Free Journey (14-years in the making!)

How We Tackle Overspending Our Budget